Adding ML-Powered Recommendations to KOHO

KOHO

ML-Powered Recommendations

CONTEXT

Image: KOHO app

This case study aims to explore the potential of implementing ML-Powered recommendations to KOHO, a leading Canadian fintech. By delivering tailored financial insights and suggestions, KOHO can empower users to make better choices and further its mission of creating financial products that are open, intuitive, and designed to help users live better lives.

In this study, I will evaluate KOHO’s ecosystem and user base to determine their common pain points. From there, I will define an MVP solution, establish success metrics and a rollout plan to test the MVP solution with a subset of KOHO users to ensure a smooth implementation.

If KOHO implements ML-powered recommendations, then its customers will make better financial choices, such as increasing savings, reducing debt, and making more informed spending decisions.

HYPOTHESIS

Technology

Enhancing UX with

Intelligent Recommendations

Recommendation engines are tools that suggest content to users by predicting what they might like based on algorithms. They go through data to show relevant information, improving user experience. The effectiveness of these engines depends on how well they understand relationships between items, users, and preferences. Different methods, like content-based filtering (focused on item features) and collaborative filtering (based on user interactions), are key to making accurate and relevant recommendations.

-

Predicts what a user will like by analyzing their behavior and comparing it to similar users. It groups users or items together based on their interactions to make recommendations.

-

Uses machine learning to train models for making predictions, like guessing a user's top-5 favorite items based on past interactions. It's better than memory-based filtering for recommending more items to more users.

-

With filtering according to content, similar items are grouped together based on their features. (e.g., their genre, product type, color, or word length). It’s what powers recommendations like "If you liked this, you might like that."

-

A recommendation engine that uses hybrid filtering utilizes both collaborative and content-based data. Not surprisingly, its superior filtering produces the best information.

Source: Algolia

MARKET

What can we learn from leading players?

ML-powered recommendations come in many forms and serve different purposes, but they all share a common goal: making decisions easier. This is crucial in a world where people are overwhelmed with information and often struggle with analysis paralysis. Companies like NU Bank, LinkedIn, and Amazon show how recommendation engines are leveraged in Fintech, and across many industries.

Amazon

Hybrid Recommendations Pioneer

When searching for the book Inspired: How to Create Tech Products Customers Love by Marty Cagan on Amazon, two types of recommendation filters are used. The "Customers who bought this item also bought" section utilizes memory-based collaborative filtering, suggesting titles like Empowered and Transformed by the same author, based on similar user purchases. Meanwhile, the "More items to explore" section employs content-based filtering to recommend other relevant product management books.

Amazon

User-Driven Personalized Recommendations

LinkedIn primarily uses Collaborative Filtering to recommend job opportunities. Based on my past applications and interactions, the platform sends notifications about relevant openings. It also considers my location (Toronto) and demographic information, like previous employers, to suggest positions in companies where similar people have been hired, especially when I'm browsing my timeline.

Youtube

Best-in-class Predictive Engines

YouTube uses model-based collaborative filtering to predict which videos users will watch next. To improve the accuracy of these predictions, YouTube occasionally prompts users to provide feedback on the relevance of the recommendations, using this input to fine-tune its algorithm.

Youtube

Nubank

Drawing Inspiration from the World’s Largest Neobank

Nubank utilizes both Collaborative and Content Filtering in its personalization engine, setting itself apart by focusing on enhancing user experience rather than just driving revenue. Unlike many companies that use recommendations to boost sales, Nubank’s primary goal is to help users make better financial decisions.

Each recommendation is tailored to individual financial profiles, offering insights like payment reminders, savings suggestions, and product recommendations based on user behaviour. What truly differentiates Nubank is its emphasis on solving user problems and prioritizing recommendations that improve financial well-being over promotional offers. Additionally, recommendations are contextually relevant, appearing only when they matter most, such as during unusual transactions or near bill deadlines. This approach ensures that even new users receive a personalized, non-intrusive experience.

NU Bank

KOHO’s customers are mostly Canadians who live paycheck to paycheck, making up over half the population. Many of these users have limited access to traditional banking services or none at all. With over a million users, KOHO targets younger, tech-savvy individuals, especially those aged 18-35, who want easy-to-use financial tools to help them build credit and manage their money better. Unlike traditional banks that focus on wealthier clients, KOHO is dedicated to providing products that help Canadians and newcomers start building wealth.

Source: Betakit

Who uses KOHO?

AUDIENCE

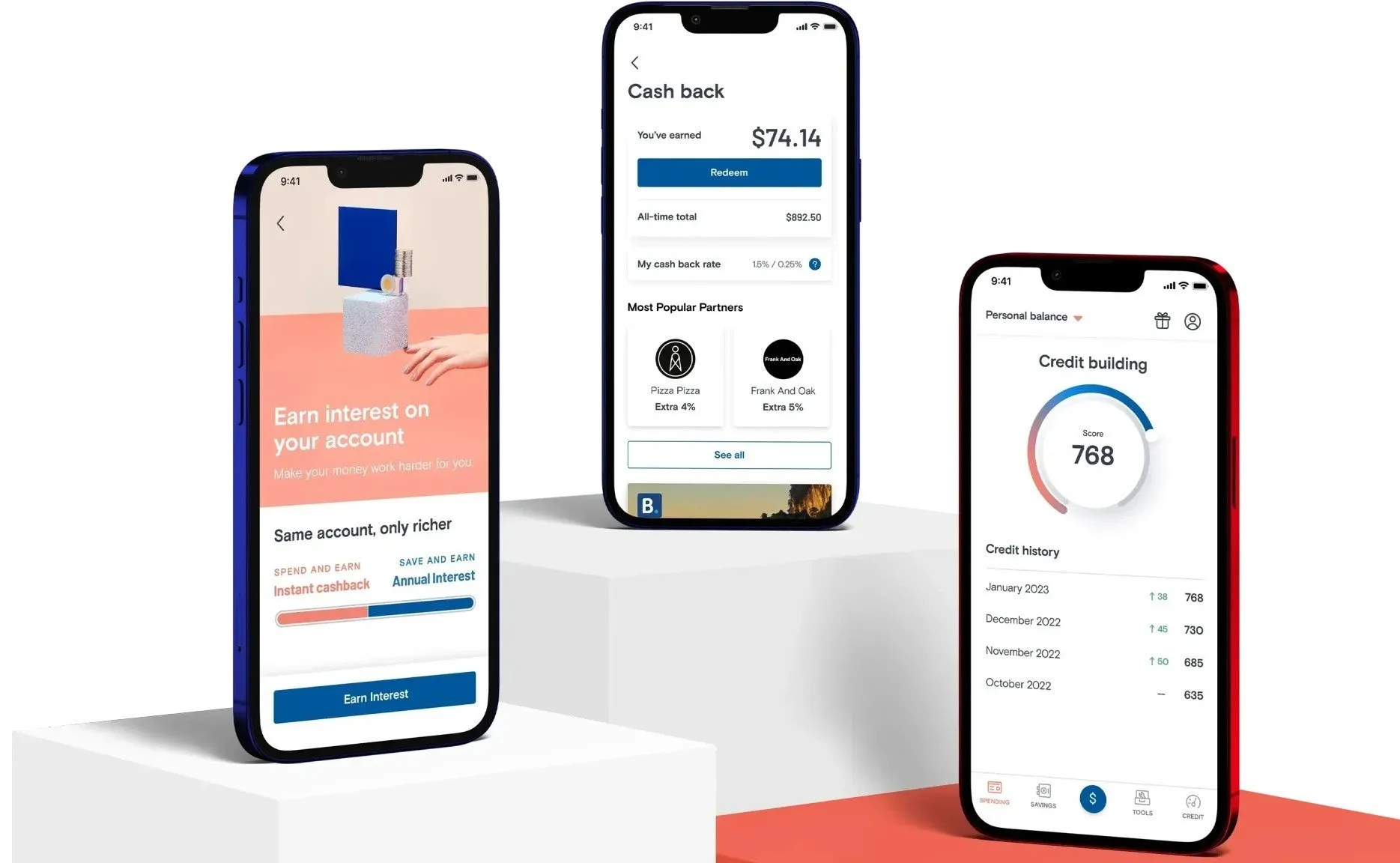

KOHO Features and Services

KOHO Mastercard:

Prepaid Mastercard: A reloadable prepaid card that works like a debit card but is accepted wherever Mastercard is used.

Virtual Card: A digital version of the KOHO card for online purchases or mobile payments via Apple Pay, Google Pay, and Samsung Pay.

Cashback:

Purchases: Earn up to 2% cashback on everyday categories like groceries, transportation, and dining, and up to 5% with select partners.

Cash Back on Rent: Earn 0.25% cash back on rent payments.

Spending and Budgeting Tools:

Real-Time Spending Insights: Track spending with instant notifications and insights to help users manage their money.

Spending Categories: Breakdown of expenses by categories to help users see where their money is going.

Interest and Savings:

Interest: Earn interest on the full balance in your KOHO account, varying by plan.

Savings Goals: Set and automate contributions toward specific financial goals.

Round-Ups: Automatically round up purchases to the nearest dollar, saving the difference.

Credit Building:

Credit Building: A tool to help improve your credit score, with average gains of 20 points in six months.

Credit Score: Monitor your credit score within the app, with insights on how to improve it.

Rent Reporting: Report rent payments to credit bureaus to build credit.

Transfers and Payments:

Bill Payments: Pay bills directly from the KOHO app.

Split Bill: Share expenses with others through the app.

Request Money: Request payments from friends or family with a few taps.

Free e-Transfers: Send and receive money via Interac e-Transfers without fees.

Loans:

Cover: Access a cash advance of up to $250 for short-term needs, no credit check required.

Pay Later: Flexibility to pay eligible purchases in smaller monthly payments.

What KOHO users are saying on Reddit?

What are the pain points that these users need addressed?

USER INSIGHTS

Main Issues

Information Overload

Users face an overwhelming number of products, services, and options within the app.

Too many options presented at once, causing confusion, distractions and decision fatigue.

Poor Onboarding

New users often struggle to understand the full range of features the app offers.

This lack of guidance can result in underutilization of the app’s capabilities.

User Interface & Experience

Users may find it difficult to locate specific features or services within the app.

This can lead to frustration and a poor user experience, particularly when in need of something specific.

Additional Concerns

Security Concerns

Users worry about the safety of their personal and financial data within the app.

Users worry about the possibility of their accounts being hacked or their personal information being stolen.

Financial Concerns

The fear of hidden fees or unexpected charges can deter full engagement with the app’s features.

Users living paycheck to paycheck may experience constant pressure and anxiety about managing their finances, which can lead to avoidance behavior in engaging with financial tools or making decisions.

Negative Past Experiences

Users with negative experiences from other fintechs or traditional banks may approach KOHO with distrust.

Frustration from being constantly targeted with ads or promotional offers in other banking or fintech apps, leading to skepticism about KOHO’s intentions.

The KOHO user journey can be distracting and confusing

USER JOURNEY

The KOHO app's layout can sometimes feel overwhelming and hard to navigate. With so many services and products packed in, important user paths can get buried, making it tricky for users to find what they need and stay on track with their financial goals. This can lead to a more scattered and distracting experience than intended.

Scenario:

Emily uses KOHO to pay for online subscriptions, her rent, and to shop through the app to earn cashback from partner deals. Last week, she ran short of cash and borrowed $200 using Cover. She doesn’t realize, though, that her current balance won’t be enough to cover the loan repayment, rent, and all upcoming subscriptions due in a couple of days

Expectations:

Check her balance

Review her savings goals

Ensure she’s managing her spending effectively

BIG TAKEAWAYS

BIG TAKEAWAYS

From this research, we can conclude a couple of things:

KOHO users are typically busy young Canadians who live paycheck to paycheck, making it challenging for them to stay on top of their personal finances.

The wide range of products and services KOHO offers can sometimes feel overwhelming, leading to decision fatigue or distractions that pull users away from their financial goals.

Leading tech companies and fintechs are increasingly using recommendation engines to help make decision-making smoother and easier for their users.

PROBLEM

KOHO lacks an easy way to remind customers about important actions that will help them make better financial decisions.

Improve KOHO users' financial health by displaying

personalized recommendations tailored to each user’s behaviour and financial needs.

GOAL

Our focus is on addressing core pain points through an ML-powered recommendation engine, which will remind users to deposit or transfer funds to their spending balance before upcoming charges. This approach will help KOHO achieve its mission of providing financial products that are intuitive, accessible, and designed to help users live better lives.

What should be included in the MVP?

FEATURE PRIORITIZATION & MVP DEFINITION

Building a Personalized Recommendation Engine that covers all content across the KOHO app is a big project. To make sure it’s worth the effort, we’re starting with an MVP of Personalized Recommendations. If it proves successful, we’ll continue developing a robust engine that supports users with targeted insights, like bill payment reminders, saving suggestions for future goals, flagging suspicious charges, and offering relevant products and services tailored to individual behavior.

-

We will introduce personalized recommendations on the Home Screen that alert users about upcoming bill payments that may impact their spendable balance.

-

Users will be redirected to a screen displaying upcoming bills.

They will see a summary of their total balance, including spending account and savings.

KOHO will suggest the minimum amount needed to transfer to maintain a positive spendable balance in the coming days.

-

Users will have quick access to a button that directs them to the Add Money screen.

The feature set for our Personalized Recommendation Engine will focus on upcoming bill payments that can be denied due to insufficient funds because:

These recommendations are highly contextual and personalized, allowing us to test whether they effectively address meaningful pain points and positively impact users' financial well-being.

They are easily distinguishable from promotional offers and other nudges users encounter in the app.

Additionally, querying multiple data sets across KOHO’s ecosystem presents a significant technical challenge. To keep the scope manageable, other personalized suggestions mentioned for future iterations have been deprioritized for this MVP.

User Stories

ML-Powered Recommendations View

FINAL SOLUTION

What risks could KOHO face by integrating ML-powered recommendation engine into the app?

RISKS & TRADEOFFS

Visibility and Usability

Adding personalized recommendations to the Home Screen can boost engagement by highlighting important insights. However, this might push other content down, making it less accessible. To avoid this, we need to monitor and measure the impact on engagement with content that may become less visible.

Respecting Privacy

Personal finances are sensitive, so recommendations must be delivered in a way that doesn’t feel invasive. Clear communication is key—users should understand why they’re seeing a recommendation and how it benefits them. It's also crucial to get the right permissions and offer an opt-out option, ensuring users feel in control.

Balancing Goals

While the focus is on improving financial outcomes, we must consider how this might impact other areas, like cashback partner spending or the use of services like Cover. It’s important to measure whether improvements in one area might negatively affect another and maintain a balanced approach.

Managing Resources

Implementing ML-powered recommendations adds complexity to the app, requiring significant resources for both the initial build and ongoing maintenance. As the app grows, supporting more features will demand additional resources, so careful planning is needed. Committing to this initiative also means fewer resources for other potential improvements, so we must weigh the long-term benefits carefully.

MEASURING SUCCESS

Core Metrics

NORTH STAR METRIC

Reduction in Declined Pre-Authorized Payments Due to Low Balance.

If we are effectively addressing our users' main pain points, we should see a reduction in declined pre-authorized payments due to low balance. This metric serves as a key indicator of success by measuring how well our personalized recommendations help users maintain a positive balance. By focusing on reducing insufficient balances, we ensure that users are better able to manage their finances.

Success Metrics

These metrics will help us identify areas within the Personalized Recommendations feature that we can further improve or optimize to reduce the number of declined pre-authorized payments due to low balances.

App Open → Core Recommendation Action Completion Rate Within a Session

Does the presence of personalized recommendations encourage users to complete core actions (e.g., transferring funds) within the same session? Are users more proactive in managing their finances as a result?

Home View → Recommendation Interaction Rate

How many users engage with the personalized recommendations on the Home Screen?

Is the recommendation clear and compelling enough to prompt user action?

Recommendation Interaction → Abandonment Rate

How many users begin interacting with a recommendation but then abandon the process without completing the suggested action?

Counter Metrics

Since personalized recommendations will play a key role in shaping the user experience, it’s essential to ensure they don’t negatively impact other critical performance metrics. To monitor this, we will track:

Decreased Product Engagement Rates

Are fewer users engaging with other KOHO products, such as signing up for credit building, creating savings goals, using Cover, or exploring partner deals, due to the focus on personalized recommendations?

Decreased Average Transaction Volume

Are we unintentionally reducing the amount of money users are transacting through KOHO by introducing personalized recommendations?

Frequency of Recommendation Engagement

Are users consistently engaging with the recommendations over time, or does engagement drop off after initial interactions?

Impact on Related Features

Are users using related features like fund transfers or bill payments more often as a result of these recommendations?

Deposit Growth Rate

Is the amount of money being transferred into users' KOHO accounts increasing over time?

Individual Transaction Volume

Is the user's total transaction value going up or down over time?

Increased Opt-Out Rates for Personalized Recommendations

Are the number of users opting out of receiving personalized recommendations increasing MoM?

A/B Test

LAUNCH & GTM STRATEGY

To ensure the ML-Powered Recommendations enhance the KOHO app’s user experience, we will conduct an A/B test. This test will involve a small group from our target segment.

-

Control: 90% of the targeted audience. (No Recommendations)

Variant: 10% of the targeted audience. (Exposed to ML-Powered Recommendations)

-

Users who:

KOHO clients who live in Toronto

Are in the 25-35 age bracket

Actively pay bills and deposit funds into KOHO on a monthly basis

-

App Open → Core Recommendation Action Completion Rate

We will begin the A/B test with 10% of our target audience, allowing us to iterate without impacting the majority of users.

If the A/B test results are positive (achieving our primary success metric with minimal negative side effects), we will expand the test to all users in Ontario, regardless of age. Should the metrics remain positive, we will proceed with a full rollout to all users across Canada.

Following a successful rollout, we will enhance the ML-Powered Recommendations by adding features from our roadmap. Eventually, we aim to provide holistic financial advice based on comprehensive user data once Open Banking is implemented in Canada.

Note: If the A/B test results are negative, we will analyze the issues, make necessary adjustments, and re-run the experiment.

Future Possibilities for ML-Powered Recommendations

FUTURE ITERATIONS

-

The AI could aggregate data from multiple financial accounts through open banking, offering more holistic and accurate recommendations that consider the user's entire financial picture, not just their KOHO activity.

-

Once Open Banking is available, offering personalized strategies for paying down debt more effectively, such as suggesting the most efficient order to pay off credit cards based on interest rates and outstanding balances.

-

Providing insights into potential cash flow issues before they happen, based on patterns in income and spending. The AI could alert users to tighten spending in months where expenses are likely to exceed income.

-

Recommending specific investment opportunities based on a user’s financial behavior, risk tolerance, and long-term goals. For example, the AI could suggest putting excess savings into a low-risk investment fund.

-

Setting up reminders for key financial milestones, such as reaching a savings target, paying off a loan, or renewing an expiring subscription, based on user-specific financial journeys.

-

Detecting and analyzing recurring subscription payments based on debit/credit card transactions.

-

Automatically recommending and transferring funds to an emergency savings account based on surplus balances or predicted upcoming expenses.

-

Identify surplus funds in a user's account and suggest automatically transferring them into a savings goal, such as a vacation fund or a down payment for a house, ensuring users steadily work towards their long-term objectives.

-

Recommending specific investment opportunities based on a user’s financial behavior, risk tolerance, and long-term goals. For example, the AI could suggest putting excess savings into a low-risk investment fund.

-

After users interact with a recommendation, the AI could ask for feedback on its relevance and usefulness, allowing for continuous refinement of the recommendation engine to better meet user needs.

Final Thoughts

Final Thoughts

SUMMARY

In this case study, I recommend A/B testing an MVP of ML-Powered Personalized Recommendations with the goal of reducing the declined pre-authorized payments for KOHO users. This MVP is designed to address core financial management challenges that users in our target segment face, such as managing upcoming bill payments and maintaining a positive balance.

If the test results are positive, I suggest expanding the functionality of ML-Powered Recommendations, eventually rolling out the feature to all users across Canada. Future enhancements could include leveraging Open Banking data, offering savings suggestions for future goals, and providing tailored financial product recommendations based on user behavior.

Thank you for reviewing this case study!